Explore strategies for

Property Owners or Buyers

Overview

Multi-family Unit

Manufactured Home

Farm/Ranch

Historic Property

New Construction

Overview

Just one inch of flood water can cause more than $25,000 in damage to your home or building. Additionally, research shows that for every $1 invested in flood mitigation, $6 are saved in post-disaster recovery costs. Given this data, it is important for property owners in flood prone areas to understand mitigation – or flood risk reduction – and what mitigation actions they can take today to reduce their risk of flooding and flood damages in the future.

This website was built with property owners and property buyers as the primary target audience. Each aspect was crafted with the individual property owner in mind. It can help you:

- Better understand flooding and flood risk.

- Explore potential mitigation options.

- Narrow down which mitigation options would work best for the property you are looking to purchase.

- Find answers to questions around flood risk, mitigation, flood insurance and financial assistance.

Owners of certain types of properties may be limited in which mitigation options they can undertake or have different requirements to which they must adhere. If you own one of the special property types listed below, jump to the associated section to learn more before proceeding. Otherwise, we recommend you proceed to the guided search.

Multi-family Unit

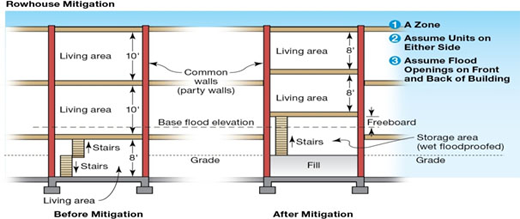

For the purposes of this website, the term multi-family unit encompasses units of both attached single-family homes (connected row houses, townhomes, brownstones, duplexes, or other multiplexes) and multi-family buildings (low-, mid- or high-rise). The key feature of each of these unit types is the shared walls, interior or exterior. Because of these shared walls, multi-family buildings are somewhat limited in which mitigation options they can pursue. For example, elevation and acquisition are generally not possible without the agreement of all owners in the building or block, and even then often not feasible given the building’s size, structural characteristics, or location, usually on narrow city streets. FEMA has developed specific guidance for multi-family units.

- If you own a unit in a building managed by a community association, check your governing bylaws or ask your building’s board president or manager to determine who is responsible for damage to your unit due to external flooding.

- If you own an attached single-family home or a low-rise multi-family building, check out Reducing Flood Risk to Residential Buildings That Cannot Be Elevated; note, however, that most techniques presented in this publication are not appropriate for high-risk flood hazard areas subject to wave action (V zones and coastal A zones) or high velocity flow areas (areas subject to alluvial fan flooding, flash flood, mudslide, erosion, or ice jam).

- If you own a mid- or high-rise multi-family building, check out National Flood Insurance Program Flood Mitigation Measures for Multi-Family Buildings; note that each technique presented in this publication identifies in which flood condition the technique is and is not appropriate.

Manufactured Home

Manufactured homes are those constructed offsite, transported over roadways, and then installed onsite, not including recreational vehicles.

Siting is critical to the successful installation of a manufactured home; when siting, you want to closely consider a property’s vulnerability to flooding if you are in a flood prone area. Once you have your site selected, you want to make sure your manufactured home is installed according to NFIP and local floodplain management regulations to prevent flotation, collapse, or lateral movement of the structure.

If your existing manufactured home is subject to flooding, you may want to look at relocating it or familiarize yourself with evacuation options in your community. Some communities and the NFIP may provide limited assistance to move your manufactured home offsite to protect it from the risk of flooding.

Additional Resources

Section 3.8 focuses on flood mitigation options for existing manufactured homes in flood hazard areas.

Farm/Ranch

Farms and ranches at risk of flooding have been given special consideration by FEMA with regard to the requirements they must follow under the National Flood Insurance Program (NFIP) – but only for agricultural and accessory structures. If you are a farmer or rancher looking to:

- Mitigate flooding of an agricultural or accessory structure, check out the construct an elevated farm pad mitigation strategy page or FEMA’s Floodplain Management Requirements for Agricultural Structures and Accessory Structures

- Mitigate flooding of a structure in which one or more people live, proceed to the Guided Search and choose single-family residence.

- Find other flood mitigation related resources targeted to farmers or ranchers, check out these resources.

Additional Resources

Historic Property

Historic properties at risk of flooding have been given special consideration by FEMA with regard to the requirements they must follow under the National Flood Insurance Program (NFIP). These considerations afford leeway to historic property owners in order to preserve these assets and maintain their historic character and integrity for future generations.

At the same time, historic property owners must adhere to strict guidelines when undertaking mitigation efforts in order to preserve their property’s historic designation. If the structure is altered in such a way that its historic character is changed, the property’s designation may be at risk.

Additional Resources

New Construction

This website was built for property owners looking to mitigate against flooding of existing buildings. Existing buildings were often built to different, lower, floodplain management standards than those required of new construction today.

If you are constructing a new building in a flood prone area, you must comply with all current NFIP and local floodplain management regulations. Your best course of action is to contact your local floodplain management official and a registered design professional in your community.

Please note that for flood insurance purposes, the term “New Construction” refers to “Buildings for which the “start of construction” commenced on or after the effective date of an initial Flood Insurance Rate Map (FIRM) or after December 31, 1974, whichever is later, including any subsequent improvements.”

Additional Resources

For information on who to contact and what questions to ask them